In property and fire insurance, some risks are considered so severe that insurers do not merely acknowledge them — they regulate them through strict policy warranties.

Petrol and mineral oils fall into this category. These substances are highly flammable, volatile, and capable of causing catastrophic fire losses when improperly stored or handled.

This is where the Petrol & Mineral Oil Warranty (PMOW) becomes critical.

What Is the Petrol & Mineral Oil Warranty (PMOW)?

PMOW is a warranty within a property or fire insurance policy that governs:

- Whether petrol or mineral oils may be stored on the premises

- The quantity permitted

- How the substances must be handled and controlled

In simple terms, the warranty means:

Your insurance cover remains valid only if storage and handling comply strictly with the policy terms.

Why Insurers Treat Flammable Liquids Seriously

Fire involving petrol or mineral oils escalates rapidly. Once ignition occurs, losses can spread quickly, causing severe damage to buildings, stock, machinery, and neighboring properties.

From an underwriting perspective, poor fuel control significantly increases exposure. As a result, insurers:

- Restrict quantities allowed on-site

- Enforce strict storage standards

- Require ventilation and fire protection controls

- Treat compliance as material to the risk

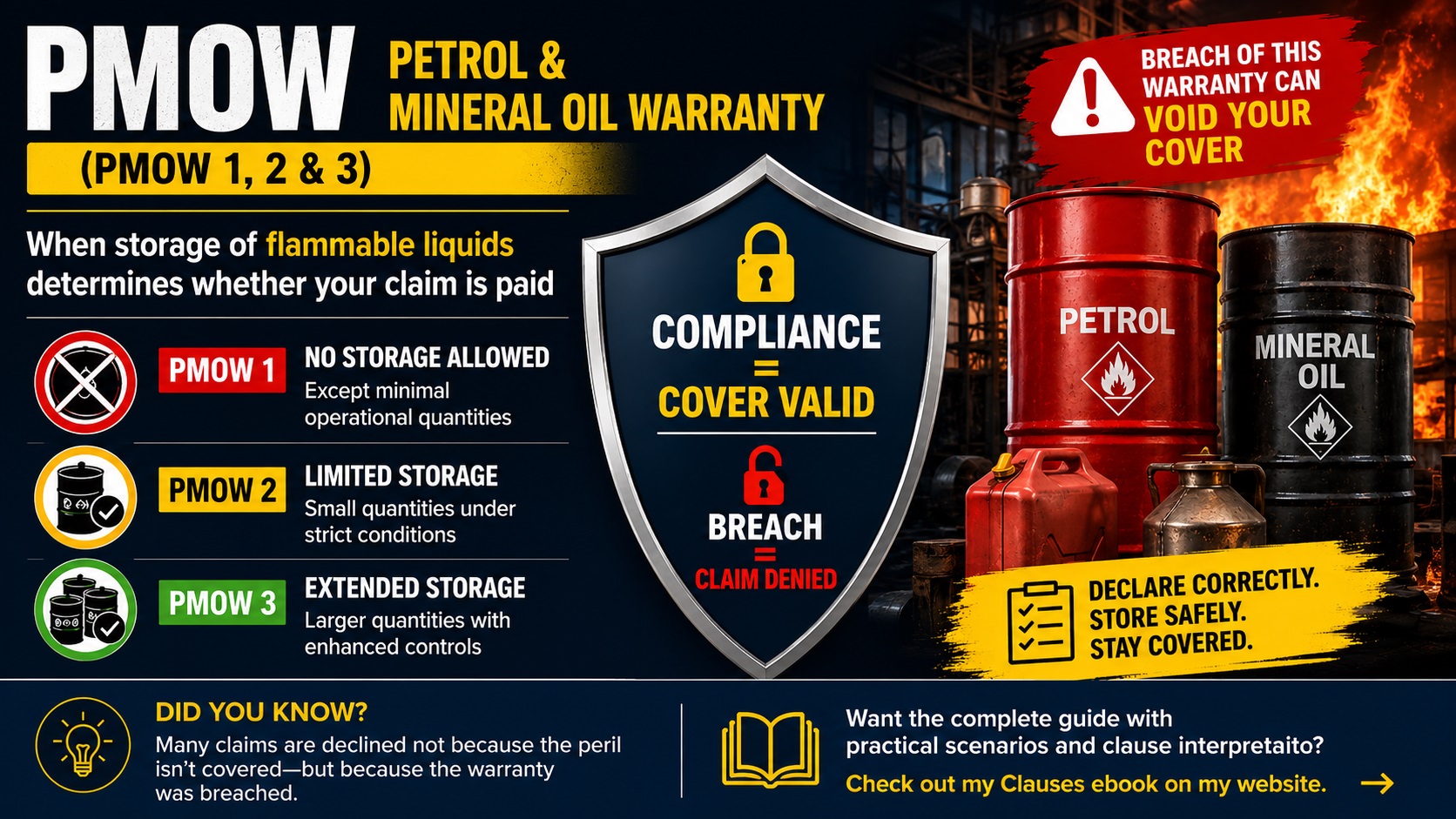

The Three PMOW Levels

PMOW 1 – No Storage

Under PMOW 1, storage of petrol or mineral oils is prohibited except for very minimal operational quantities.

This category is commonly applied to:

- Office buildings

- Low-risk commercial premises

- Businesses with no industrial fuel exposure

Any significant storage beyond minimal operational use may constitute a breach of warranty.

PMOW 2 – Limited Storage

PMOW 2 permits storage of small quantities of petrol or mineral oils, subject to strict controls.

Typical requirements include:

- Approved storage containers

- Adequate ventilation

- Safe placement away from ignition sources

- Compliance with quantity limitations

This level is commonly used for workshops, garages, and moderate industrial operations.

PMOW 3 – Extended Storage

PMOW 3 allows larger quantities of flammable liquids but requires significantly enhanced controls.

These may include:

- Designated fuel storage areas

- Fire suppression systems

- Compliance with safety and regulatory standards

- Enhanced risk management procedures

This category is commonly associated with industrial facilities, fuel depots, and operations involving substantial fuel use.

How PMOW Works in Practice

At policy inception:

- The insured declares fuel quantities and usage

- The insurer assesses exposure

- The appropriate PMOW category is applied

During the policy period, the insured must comply fully with the warranty conditions.

Any deviation may result in:

- Claim denial

- Reduced settlement

- Policy avoidance in severe cases

The Critical Distinction: Warranty vs Condition

One of the most misunderstood aspects of PMOW is that it is a warranty, not merely a policy condition.

This distinction is legally significant:

- Conditions may allow some flexibility

- Warranties require strict compliance

A breach of warranty can affect claim validity even where the loss itself is unrelated to the breach.

Practical Examples

Example 1: Office Fuel Storage

An office premises insured under PMOW 1 stores multiple fuel containers for generator use beyond permitted operational quantities. A separate electrical fire later damages the premises.

Result:

- The insurer may treat the undeclared fuel storage as a breach of warranty

- The claim could be declined despite the fire not originating from the fuel

Example 2: Compliant Workshop Storage

A workshop insured under PMOW 2 stores lubricants and fuel within approved quantity limits using compliant containers. A fire occurs due to welding operations.

Result:

- The insured complied with warranty requirements

- The claim is more likely to be payable under policy terms

Example 3: Industrial Site Exceeding Declared Limits

An industrial site insured under PMOW 3 gradually increases on-site fuel storage without notifying the insurer. A fire later spreads rapidly due to the excess fuel load.

Result:

- The insurer may reduce or deny the claim due to material breach of warranty

- Failure to disclose increased exposure becomes critical during claims assessment

Why This Clause Matters

In practice, fuel storage is often handled informally. Quantities increase gradually, safety controls weaken, and disclosures are overlooked.

Many insureds assume that because fire is covered, all resulting losses will automatically be paid. However, property insurance is not based solely on the occurrence of a peril — it also depends on compliance with warranties and risk controls.

This makes PMOW one of the most important operational warranties within property insurance.

Go Deeper: Master Insurance Clauses

The Insurance Clauses Ebook breaks down real-world policy wording, underwriting intent, practical claim scenarios, and critical interpretations used in actual insurance practice.

View Energy EbookKey Takeaways

- PMOW regulates storage and handling of flammable liquids under property insurance.

- The warranty defines whether storage is prohibited, limited, or extensively permitted.

- Strict compliance is required because PMOW is a warranty, not merely a condition.

- Breaches may lead to claim denial even if the loss is unrelated to fuel storage.

- Proper disclosure and risk control are essential for maintaining valid cover.